Weekly FI ETF Report: Dr. Bernankenstein & Catch 22

Dr. Bernankenstein

I can’t help but think of Dr. Frankenstein with his experiment that goes wrong. An experiment, that seems to have no hope of succeeding, but then does, but then doesn’t play out according the script.

Whether Ben can continue to look at the latest “unlimited” QE without questioning it remains to be seen, but some within the Fed and possibly even Treasury must be wondering what sort of monster he has created.

The markets are not responding “normally”. No matter whether you are bullish or bearish we are seeing moves that seem completely out of proportion to the news. IBM, Apple, Google, and Netflix were just three striking examples.

Markets do seem to have strength and one day it is “good data” that propels us forward, then we ignore bad data because “housing is good” and then we ignore data that indicates housing isn’t so good because we can.

It is impossible to have a conversation about the markets without discussing QE in one form or another. The ECB has mostly threatened to do it, Japan has entered a new and more aggressive wave, but it is really the Fed’s policy that is pushing the markets the most.

$100 billion a month of purchases (sure it isn’t quite that big, but what is $15 billion or so a month between friends). The enormity of that purchase program is changing market behavior. Obviously Ben has a plan and that plan is to push investors and business back into risk taking that leads to job creation and then housing growth and then economic nirvana.

That is his plan and over the past 6 years (aggressive Fed started back in 2007) it has met with some success, at least in supporting markets, but less obvious success in creating real economic growth. We will never know if a different plan would have worked better by now, because that path was never followed, all we know is what Ben’s plan is supposed to do.

The problem is the plan may not be working. It may be creating risk appetite in financial assets without real economic growth. Sure, I’ll buy stocks because the Fed is buying bonds, but I’m not about to build a new widget plant, because the Fed isn’t buying widgets.

It is hard, at least for me, to look at the past 2 weeks as being “normal” in any sense of the word. Market psychology is changing. Valuation and risk are battling it out as least used terms in the market. The biggest fear seems to be of missing the rally, that this time the Fed has really found a way to push everyone over the edge.

I’ve been wrong before, and I’ll be wrong again, but usually I can easily understand why I was wrong about. I expected good data and bad data came out. I thought the tax selling was overdone, but fears of tax hikes increased and I missed how overbought something was. Right now, I am wrong, and the bulls don’t seem to want to articulate a real argument. Just because of QE is enough. Just because [insert positive here] in spite of at least some evidence the positive doesn’t exist.

Some Fed members questioning the need to be aggressive in September. It seems like there has been at least some growth to the opposition in each subsequent meeting, in spite of the Fed actually getting more aggressive. I think there must be people at the Fed getting concerned that it has gone too far and they are changing investment behavior in a way they didn’t intend to and might be unleashing something worse than what they were trying to avoid.

Has QE become too sexy by far?

Right Said Fed

One question that is coming up more frequently is “what did the Fed say”. The Fed said it would tie policy to unemployment and possibly inflation (though no one seems to believe the inflation target). Some members of the Fed seemed to indicate that the targeting was in relation to “low short term rate” commitment. The consensus seems to be that it applies to both the short term rate commitment and to the asset purchase program.

Since I already interpret some Fed comments as a way to separate those two and to tie only the short term rate commitment, I think the market could be in for a surprise. Maybe someone at the Fed will get worried enough about the apparent distortions they are creating in the markets with their asset purchases that they will dial them back a bit?

The Market’s Catch 22

The week ended with stocks rallying and bonds selling off. The problem, at least as I see it, is that can’t last for long. One version of the bull case is:

- Low rates encourage business to borrow to grow

- Low rates helps consumers spend and lets the housing market do better

- Growth and housing doing better is very good for stocks

- Rates go higher as investors move from bonds to stocks

It is that last link that strikes me as contradictory. If low rates are one of the key reasons for the market to get excited, the virtual “certainty” that rates should be going higher seems to be a direct contradiction. Won’t rising rates (if they happen in a meaningful way) not only stop the stock market rally (discounted cash flow and relative value both affected)?

In the past 4 years, credit spreads could contract enough that even if treasuries rose, the yields on most loans (corporate, real estate, or individual) could move lower while treasury yields rose. The “risk” component of the risky bonds could offset that rate move while risk (including equities) did well. That CANNOT happen this time.

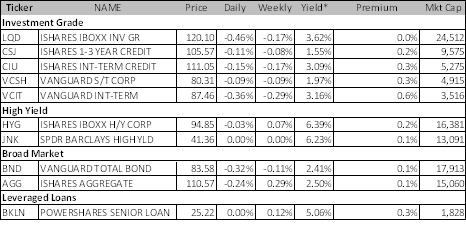

High yield, as measured by HYG, is up less than 1% since the January 2nd close. LQD (a proxy for investment grade bonds) is down since then. So while stocks have rallied, the borrowing cost for corporations has not improved much this month. That is different than in prior periods of QE. Municipalities have fared better, but still not getting the big benefit.

The U.S. Government has almost $3 trillion of debt maturing in 2013, all of which will need to be replaced, plus some. Every 1% increase on just the debt that gets rolled would cost us $30 billion (I’m ashamed to admit, but I used a spreadsheet on that calculation because it just seemed too large). So a 2% move higher on the cost of the debt we roll would cost as much as a hurricane Sandy.

I’ve been reading some reports that attempt to explain why stocks can do well with rising yields, but so far I haven’t found them convincing. Not when so much of the move seems predicated on low yields.

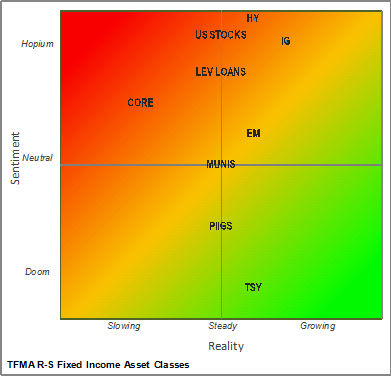

Sentiment versus Reality, or What is Priced In

Our assessment of what the real outlook is for various asset classes versus our sense of how people are positioned. Red indicates overvalued, Green is undervalued, and Yellow, is neutral. It isn’t exact. In our view, positioning and sentiment is more important, at least from a contrarian view. While it is possible to have strong support for an asset class with strong fundamentals still be a “buy” it is far more common to see sentiment diverge from reality and that is the opportunity.

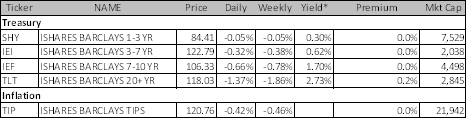

A Darker Shade of Gray for Treasuries

It may not have been a Black Friday for Treasuries, but it was pretty bad. They sold off throughout the entire day with no real respite. The long bond had gotten back to 3% at one point on Thursday, and from there was met with nothing but selling.

Ironically, or at least I think it is ironic, the “reflation” crowd treated TIPS almost as badly as other bonds. So there is real risk of inflation, except in the product that pays out based on inflation? More of the strange trading I see.

While depressing to go from smart and right, to back to stupid and wrong on treasuries in 36 hours of trading, I remain dubious of the sell off and think treasuries are still meant to be added to here on weakness.

The Synthetic CDO Countdown is On

Before reading this section, look at the performance of the “credit” ETF’s. Anyone surprised that many were negative and while HYG eked out a small gain, JNK couldn’t even do that? Bank debt did well, but at least in part because people aren’t paying close attention to what it really is (LIBOR floors for example limit initial impact of any rise in rates).

So, the chase for yield is on and in cash markets is running out of steam. Tenet Healthcare, albeit senior secured, issued 8 year bonds at 4.5% this week. The deal is only trading okay. What else could it really do? Slathering over 4.5% bonds of a company that has had a somewhat checkered history hardly seems the wisest strategy. So investors will turn to alternatives.

While CLO’s have done well, even there the value is starting to be squeezed out. As underlying loans get tighter, as companies shift to the bond market to lock in rates, rather than being exposed to floating rates rising, the ability to create CLO’s where all parts of the capital structure are happy will decrease.

What is the one credit product that can be created at the snap of the finger? Bespoke tranches of synthetic CDO’s. You can laugh. You can crumple up this piece of paper in disgust (if you took the time to print it), but I am not joking. There are lots of issues with potential capital impact for banks, but with Basel III getting pushed off and next year’s bonus much more tangible, this is the likely path. With IG credit trading where it is, synthetic CDO’s are one of the few areas that investors can turn to in order to get yield, and heck, with the Fed pushing on all the right buttons, spread contraction could play a big part.

I don’t think this is imminent, but seems a logical progression. Just to be obnoxious, the big bank out there that is often the best contra indicators around continues to shut down “structured credit” to focus on “liquid credit”. Yeah, the thing that is transparent and moving more towards machine trading is the direction to take?

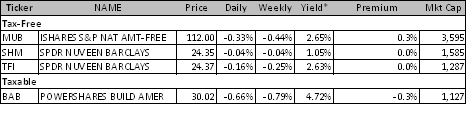

Muni’s

Rate exposure beat spread improvement last week. Some individual bonds did well, some did poorly. I remain largely indifferent on this market. I think it will have another opportunity to do very well, but need stability in treasuries and until that happens, I think these linger along. If any real rotation out of fixed income into stocks is occurring at the retail level, the only people that have the money to impact the market are high net worth individuals and big family offices, and they own a LOT more munis than they own treasuries, and hedge funds tend to avoid munis unless ridiculously cheap, because liquidity is awful, and they don’t get paid on after tax returns for their investors. Didn’t mean to sound too bearish there, I’m just neutral.

EM Bonds are NOT EM Stocks – Seriously

I just changed the title a little from last week. EM was a little weaker, but value is getting harder to spot in this market. Many of these countries are fraught with event risk and at these spreads, the chase for yield is getting old (as is my using that phrase).

I don’t look at LEMB as it remains below my $1 billion threshold, but local currency debt seems to offer some more upside. I will take a closer look, as can’t leave any stone unturned when looking for value, but EM bonds don’t seem to be the place.

German 2 Year Bonds are Known as Schatz

My favorite trade in fixed income here remains short bunds (German 10 year bonds) and long (Italian and Spanish 10 year bonds).

I won’t bore you with the details, but German bonds benefitted from hopes of being redenominated. That hope shouldn’t be getting priced in, but so far I still think it is.

Dividend Stocks as an “Other”

Nice and steady. About to add a utility component.

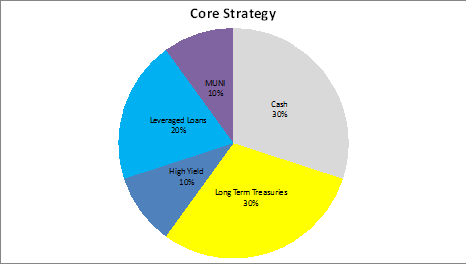

Fixed Income Allocations

The “Core” strategy is meant to have limited number of trades. It would only be readjusted as longer term views change, or short term views become very large or very strong.

This strategy would have lost 0.57% for the week bringing the YTD return to 0.39%.

Treasuries were the problem, but munis didn’t help and even leveraged loans and high yield added next to nothing. Looking at the mix here, I think we will take down leveraged loans (they seem so high) and maybe add something a little more exotic. TIPS are also getting a closer look as a way to add some risk.

The core strategy has moderate duration risk and medium high on the credit exposure.

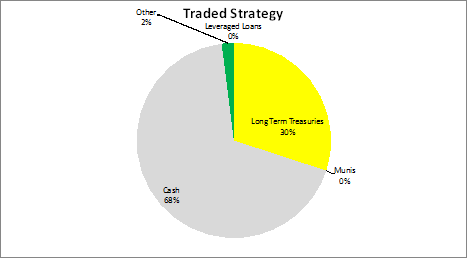

The “Traded Strategy” is meant to have more frequent rebalancing and to capture smaller moves in the market.

The traded strategy lost 0.55% last week bringing the YTD return to -0.10%.

Treasuries hurt this strategy with the entire move happening in 1 trading session. Other than maybe adding TIPS and in fact increasing some trading now that volatility is back, nothing has changed in our view, but we will watch how the technicals play out especially in the treasury market.

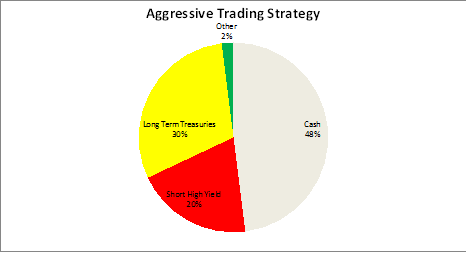

The “Aggressive Trading Strategy” is meant to be traded frequently and will expect to generate more from positioning than from yield.

The strategy lost 0.56% last week dropping the YTD return to -0.22%.

Treasuries were to blame, but high yield actually did nothing, which is encouraging for that position as stocks hit new highs and the “risk on” frenzy seemed like it should have been strong enough to take high yield higher.

The portfolio is defensively positioned.

E-mail: tchir@tfmarketadvisors.com

Twitter: @TFMkts

Disclaimer: The content provided is property of TF Market Advisors LLC and any views or opinions expressed herein are those solely of TF Market Advisors. This information is for educational and/or entertainment purposes only, so use this information at your own risk. TF Market Advisors is not a broker-dealer, legal advisor, tax advisor, accounting advisor or investment advisor of any kind, and does not recommend or advise on the suitability of any trade or investment, nor provide legal, tax or any other investment advice.