The T-Report: Lord Cliffdemort

The Name That Shall Not Be Spoken

CNBC has a “Cliff Countdown” clock. Every second interview seems to be about the cliff. Well, I am going to try and avoid it as much as possible. My post election view was that the concern was massively overdone. My view now is there is a little too little concern. I will let you know if that changes.

The Real Market Drivers

While everyone is busy focusing on the thing that shall not be named, we are seeing a strong rally in Chinese shares overnight which has dragged up other risk assets, at least for now. China is easing some investment restrictions. It seems about time that the new government tries to get off to a positive start. This move was also helped by the Chinese PMI earlier in the week.

In the meantime we have 3 days of data on the employment situation this week. Remember when employment was the key to the markets? That seems so long ago though if I check my calendar it was only 1 month ago that everyone thought employment was important. Guess what? People were right to focus on employment as it is the only way to get lasting growth.

We have ADP today, Challenger and Claims tomorrow, and then NFP on Friday. People are already making excuses about Sandy. We are acting as though collectively we can’t form an intelligent opinion on the impact of a hurricane. Is it really so hard? What portion of the country was affected? How many days? How many jobs hurt initially? Any job gains due to the clean-up? While figuring out the true underlying trend in the employment situation isn’t simple (especially since the data has a wide margin for error to begin with), it isn’t rocket science.

If we get a headline number above 150,000 it would be great for the market. You could argue that Fed policies are working. That the turn in housing is leading to more jobs. Remember, the only area that the Fed can ensure any jobs that are created are American jobs, is in housing. The stimulus in almost any other industry is as likely to lead to foreign jobs as American ones.

On the other hand, no matter how much you huff and puff and blow your hurricane stories, a negative print will be horrible for the markets. Personally I’m leaning towards a downside surprise being far more likely.

Claims have been elevated. Sales seem to be coming in light. We will find out whether an election with record spending helped fuel some of the positive numbers. I’m told it doesn’t, but I find it hard that much time and effort was spent on the election without any bump to the economy.

I am prepared to be pleasantly surprised, especially as I think the stabilization in housing is real, but I remain dubious and lead towards a downside surprise.

Hate the Vehicle not the Asset

I don’t particularly like high yield valuations here, but I think there is still some value. I generally prefer less liquid deals, smaller secured “middle market” opportunities and specific bonds of specific companies. I even like CDS here from going long credit and HY19, the on the run CDS index has several things going for it, once I get a little more bullish.

What I don’t like is HYG or JNK as an investment right now. This week in our fixed income strategy we went through the top 5 bonds in HYG. To our institutional clients we went on a deeper dive into the portfolio. My quick take is far too many of the bonds have no upside due to convexity. They are trading to relatively near term calls, and any price appreciation is capped as they move to even nearer term calls. At the other end of the spectrum, too many bonds have far too much rate risk at these yields, and will not perform well if we a get a typical “risk on” move where treasuries sell-off.

Recycled because I think it means something, though can’t quite put my finger on it

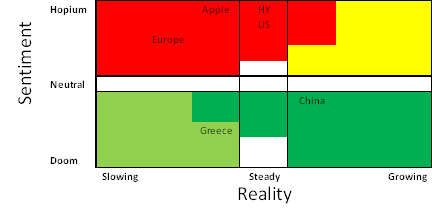

This is from yesterday and I am sending it again because I think it helps me frame my views. What is important isn’t what is currently happening, but what the market has priced in will be happening. I am still having trouble expressing what I’m trying to say. Maybe it is as simple as this chart is the Contrarian’s View of the market. I want to refine this because I think it is applicable at every level. It is clearly subjective and clearly my valuation judgment is tied into placement, but I sent it again because 1) it got very lucky in the past 24 hours, and 2) I feel I’m on to something, and the only way to improve it is to get it out there.

Disclaimer: The content provided is property of TF Market Advisors LLC and any views or opinions expressed herein are those solely of TF Market Advisors. This information is for educational and/or entertainment purposes only, so use this information at your own risk. TF Market Advisors is not a broker-dealer, legal advisor, tax advisor, accounting advisor or investment advisor of any kind, and does not recommend or advise on the suitability of any trade or investment, nor provide legal, tax or any other investment advice.