Weekly Fixed Income Summary & Strategy: Tired of the Yield Chase?

Chasing Yield Is Tiring Work – is the Market fit enough to keep going?

Well we got some chase for yield. High yield did well. EM did okay, as did Munis and Investment Grade. Closed end funds on the fixed income side did very well, benefitting from leverage and short memories, where once again investors want these at a premium (image of Homer Simpson repeatedly burning himself).

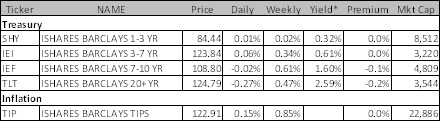

Treasuries actually had a good week in spite of the “risk on” mentality, but that was “confirmation” from Hilsenrath that the Fed is likely to continue to find ways to buy long dated treasuries once Operation Twist is officially over.

So it was a nice, and surprising combination for treasuries and risky bonds to do well, but this week was the first time in awhile that we saw some confusion in the broader market about corporate bond performance.

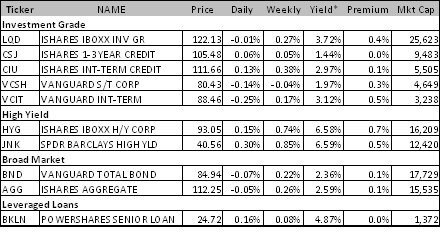

In times of stress, high yield can perform much like equities. There is a lot of upside when you are buying high yield bonds with 8% coupons and a price of 90. That is NOT the world we are currently in. Specific bond selection is key to getting any further appreciate. While that is primarily true for high yield, it is also true in investment grade. We touched on the issue of yield versus spread in You look great in Blue, buy this Pink dress.

We will look more closely at the risk and problem in the individual sections, but this is a growing focus, particularly if playing the market through “indices” or beta plays like ETF’s.

My bigger question is how much more room is there to chase yield? There is definitely more room to go, and my basic premise is that credit will continue to outperform, but there is time to be “patient” here.

Too many negatives were ignored by the market this week.

- The Greek deal is less of a deal and more of a plan than is priced in

- The market is pricing in a “successful” fiscal cliff negotiation, so the upside from a deal is mostly priced in, and the market too easily ignored the “posturing” this week, which, while I agree that it is posturing, sometimes posturing becomes reality, so concern is warranted

- Housing was generally good, and some real positives there, but away from that, the economic data seemed squishy, and there should be some concern that you can only blame so much on hurricane Sandy before someone gets nervous that the problem is bigger than that

So as a whole, it is time to dial back. Be patient. While the chase for yield is still the likely course of action, we are due for a pullback on risk assets, and fixed income will suffer. I’m not so bearish that I like treasuries, just cautious for a little, that too much has been priced in, so downside is there, and for many fixed income markets, the upside is definitely capped.

Amazing what a Buyer with Endless Capacity Can Do for a Market

Treasuries did well for one and only one reason, more Fed purchases. No one is buying treasuries in the “chase for yield”. They are buying them for a trade. If the Fed is going to buy the “belly of the curve” of 5 to 10 year bonds, then you might as well buy them too.

If you spend time this weekend reading about inflation expectations and their impact on treasuries you have just lost a few minutes of your life that you won’t get back. At some time in the future, things like that may matter, but not now. Pretending that treasuries trade the way they used to, is just wrong. There is a big buyer and every fast money trader knows it, and will go along with what the Fed is doing.

That is why the Fed will never be able to exit by selling. The moment they threatened to sell, yields would gap higher, regardless of anything else. So for now, look for treasuries to do okay. It is hard to sell off if the Fed is going to grow its balance sheet. I do think it is hard to rally much further even in a risk off moment, so am neutral here.

Credit Spreads and Yield

Generally a good week for credit spreads.

LQD, actually performed relatively poorly. It didn’t keep pace with treasuries. We did see IG19 finish the week only unchanged, which was not great performance. The reality is people had gotten too bullish on credit, then we saw spread widening in the “liquid” index, that quickly reversed itself. I think the market is a bit too aggressively positioned from the long end here (mid week I felt the opposite), so I think we can pause. The bonds may have underperformed as they dealt with supply (the new issue calendar was unexpectedly large for this time of year as companies issued debt to pay one time dividends). The bonds also lagged because they hadn’t sold off as much as they should have during the post election fear stage, so some normalization is required.

High yield did well. No complaints there but it is time to re-evaluate the strategy here. Bond selection is meaningful. It is easy to see a “risk on” market where generic ETF’s underperform. Not all high yield bonds are the same. In fact, high yield bonds are more complex than any other bond market, and many of the factors that make them attractive in general, aren’t so obvious right now.

Let’s take a peak under the hood of HYG. I am not picking on HYG, since they generally do a good job of tracking their index, it is a matter that the index itself has problems here.

The biggest holding is the Sprint Nextel 9% bond due 2018. Now that sounds good. 9% for 6 years, great! Wrong. It closed Friday at a price of 123 to yield 4.53%. There is definitely some upside left. The company has a new strategic partner, etc., but the upside gets capped. Convexity and pull to par make it harder to go up (though here I’m willing to admit that the new strategic investor could help a lot). The other issue facing this bond is the yield risk. While high yield is often not correlated with treasuries (and in many cases is inversely correlated) this bond has too much rate risk to ignore. Spread compression might not keep up with yields backing up in a “risk on” mode.

If rate risk is a potential issue with the first bond, then watch out for the next two biggest holdings, CIT 5.5% of 2019 and HCA 6.5% of 2020. Those coupons don’t even sound like high yield, and the yields those bonds are trading at are even lower. Those are both trading around 4.3% and have far less obvious catalysts for spread improvement and are going to struggle to go higher in price if yields back up.

The 4th largest holding is at the other end of the no upside spectrum. 11.25% INTEL bonds due in 2017. This sounds great until you realize that INTEL is the ticker and the company is Intelsat and not the chip manufacturer. But even still at least this looks like a high yield bond, so there must be upside? Not so much. The bonds are at 106.25 now with a yield to maturity of 9.4%. Not bad, but also, not relevant. They have a yield to call of 7.3%. These bonds are callable in February at 105.625. Could these bonds trade to 108? On cursory glance, sure, why not? They can’t. In spite of the of “juicy” coupon and the misleading final maturity, a price of 108 would produce a yield to call of -0.86%. While Germany might be able to trade at a negative yield, this bond won’t. So there is less than 2 points of upside in this bond. You would be betting against their ability to refinance this debt, which in this environment is a silly bet. And if they can’t refinance this debt because they are having trouble, or the market is weak, then the price won’t be 106.25.

The next largest holding, the FDC 12.625% bonds are better because the call risk is a bit further removed.

So that is the top 5 holdings and demonstrate why expecting a generic pool of HY bonds to perform well, even in a “risk on” environment is a dubious strategy. Individual credit selection will be important as will specific bond selection. I am not afraid of high yield, and will be in again, but the ETF’s aren’t going to gap that much higher given the portfolio they have.

If you can do it, going long HY19, the CDS index is a much better “risk on” trade. It is 100 equally weighted names with a fixed maturity, so it will outpace HYG in a “risk on” mode as it isn’t impacted by rates moving higher, and has a decent fixed duration relative to the bonds with bad convexity. If I lose you with some of those words, I apologize, but it isn’t just jargon, it is what drives returns in fixed income.

Bank loans lumber along. I like them here. Good mix of downside protection and decent carry. Almost no upside but that isn’t the purpose of owning them. CLO’s continue to get priced and done, meaning there is a deep bid to the underlying loan market.

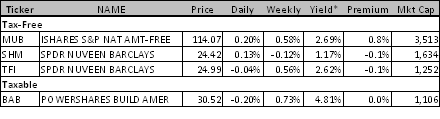

Muni’s and a lack of liquidity.

Munis did well again, and it is hard to dislike them, but I am almost at that point. Too much rate risk and far too much comfort with the credit risk. Markets are thin and an already strong seasonal time for tax purposes, made them even more attractive with fiscal cliff discussions looming, but where you can get good liquidity, it is time to lighten up with the goal of buying back. I am sadly aware of how limited that strategy is in the muni space since too few bonds have the liquidity necessary to be in and out profitably. The etf’s aren’t a bad way to play that, but I won’t call a short there yet, because I figure I have to be really right on a call that most RIA’s will say is insane. So for now, lighten up what you can, with intention of buying back cheaper, not getting out of permanently.

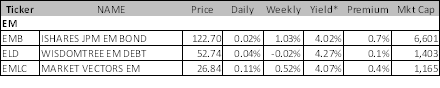

EM

EM did well again. Not surprising in a general risk on environment, but was also helped by a ruling in favor of Argentina in their long legal battle with holdouts.

Spain – No Mas

I got out too early. I didn’t see the Greek deal as being that positive. While the election in Catalonia didn’t concern me too much, I thought it might impede further strength in the market. I was wrong. I thought I was smart and lucky as on Tuesday you could sell the 3.75% November 2015 bonds at 100.6, so up on the week and ignoring what I thought was marginal, if not bad news. The bonds continue to climb, peaking at 101.5 (to yield 3.5%). By the end of the week they were back to 100.80, making me feel a little better. I still don’t like these bonds right now because too many people are acting as though things in Europe are done, and all that has happened is they have announced plans to be done, which is very different and leaves too much room for error. What I really missed is how desperate people are to believe. The 10 year bonds went from 101.75 last Friday to close at almost 104 this week. That is far too much in my opinion and will not be looking to be bullish here.

Annaly Capital as an “Other”

This stock and sector was stable this week. It is a bit disappointing that it didn’t do more this week.

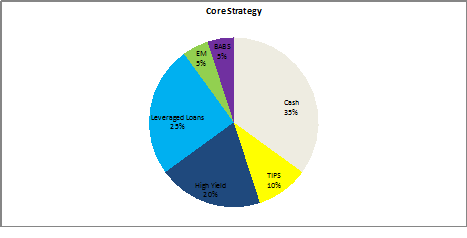

Fixed Income Allocations

The “Core” strategy is meant to have limited number of trades. It would only be readjusted as longer term views change, or short term views become very large or very strong.

This strategy would have been up 0.53% for the week bringing the 5 week return to 1.13%. The chase for yield helped this portfolio, and only leveraged loans didn’t do much.

On Friday, we announced cutting high yield exposure to 20% from 40% and taking leveraged loans from 40% to 25%.. If anything, considering cutting the EM and BABS exposure. The core strategy has moderate duration risk and medium high on the credit exposure. The “target” yield on this portfolio is now down to 3.1%.

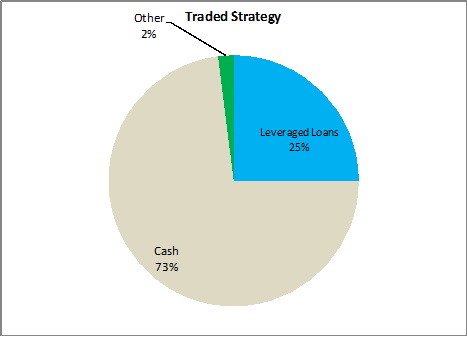

The “Traded Strategy” is meant to have more frequent rebalancing and to capture smaller moves in the market.

The traded strategy had returns of 0.22% last week bringing the 4 week return to 1.07%. The strategy was aggressively positioned coming into the week but is now positioned almost entirely in cash. The performance was dragged down by too big of an allocation to leveraged loans, and cutting half of the HY allocation too early. As mentioned already, cut Spain too early, but had we left it, the portfolio would have done virtually the same.

The expected yield of this portfolio is barely above 1% since it is mostly cash. This portfolio runs the risk of being underinvested and having to catch up in the chase for yield, but the view is that there will be opportunity to add at better levels.

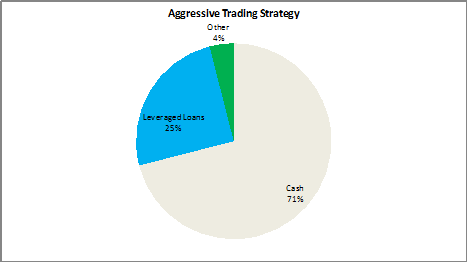

The “Aggressive Trading Strategy” is meant to be traded frequently and will expect to generate more from positioning than from yield.

The strategy should have made a disappointing 0.16% last week for a 5 week total of 1.46%.

Basically sold winners too early, including EWI which turned out okay but was removed at a 2% loss on a 2% stake. Except for an extra piece of NLY, the aggressive portfolio is now basically identical to the traded one. If anything, the aggressive portfolio is like to put on some shorts or move into treasuries as it plays for an even more aggressive risk off trade, but maybe it too will get forced into the hunt for yield at lower levels. Lack of patience hurt and too much reliance on leveraged loans doing better relative to hy than they did.

The portfolio is defensively positioned.

Disclaimer: The content provided is property of TF Market Advisors LLC and any views or opinions expressed herein are those solely of TF Market Advisors. This information is for educational and/or entertainment purposes only, so use this information at your own risk. TF Market Advisors is not a broker-dealer, legal advisor, tax advisor, accounting advisor or investment advisor of any kind, and does not recommend or advise on the suitability of any trade or investment, nor provide legal, tax or any other investment advice.