The T Report: Greece is the Word and OMT isn’t a Word

How OSI May be the End of OMT and ESM

For now we can ignore the brutal statistic of 25% unemployment. That sounds callous, and I guess it is, but that is not why Greece is going to become a key issue in the ongoing battle of European bailouts.

There is growing talk of some official sector losses for Greece. We see the denials, but the reality is the only real place for debt reduction is in the official sector.

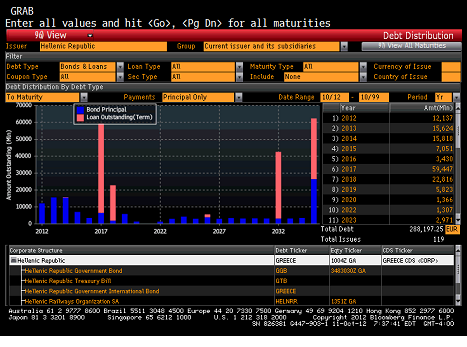

This isn’t the easiest chart in the world to read, but as I think I can walk you through it and explain why it is so important.

Official Greek Debt is €288 billion. I don’t think this includes every bilateral loan made by the EU and certainly doesn’t deal with any national central bank loans.

It does include the entire Public Sector debt. That is bonds held by actual real people or institutions and not government entities. The PSI bonds total just over €62 billion. There is about €4 billion of Greek legacy bonds documented under non-domestic law. So of the €288 billion, at most, €66 billion is held outside of the official sector.

The PSI bonds trade with an average price for the “strip” around 22.5. So there is about €14 billion in PSI market value.

Another Round of PSI Does More Harm Than Good

Greece could in theory wipe out the remaining PSI debt. There is nothing to stop them from doing this. It would be harder to wipe out the non-domestic law debt without triggering cross defaults, and since that is “only” €4 billion, let’s focus on what happens if they wipe out PSI debt. The sad truth is it wouldn’t accomplish much.

It would reduce debt from €288 billion to about €222 billion. That sounds okay on the surface, but from a practical standpoint it accomplishes next to nothing. It will save Greece about €1.25 billion annually in interest (the PSI bonds only pay 2%) for the next 10 years. That is it. The annual savings for 10 years would be €1.25 billion for a total of €12.5 billion over the period. Yes, in 2023 they won’t have to redeem the debt, but who really believes Greece will make it 10 more years if all they get is a measly €1.25 billion in current savings. They might as well print T-shirts saying “My FinMin went to the Troika and all I got was this lousy T-Shirt”.

While crushing the PSI bonds would do next to nothing for Greece’s ability to survive in the near term, it would send shockwaves through the bond markets.

Anyone left holding Spanish or Italian debt would become very afraid. If deep down you want to believe in OMT, no subordination, and that PSI was a one-time event for Europe, you would be in even greater denial of reality. Crushing the public sector in favor of the official sector once again would have severe ramifications throughout the bond investing world.

Without the ability to buy naked CDS, the only short positions would be via bonds themselves so the pressure would be immediate and direct.

I don’t see how another PSI accomplishes anything real for Greece, and the risk of spooking sovereign debt investors is real and shouldn’t be underestimated. So another round of PSI is unlikely.

If PSI Doesn’t Work, then Doesn’t OSI Have to Work?

The official sector is the only thing that might be able to work.

It is here that near term pressure can be removed from Greece. The official sector is charging a higher interest rate and is the bulk of all near term debt maturities. Since the ECB and IMF fund themselves at less than 1%, they have a lot of ability to reduce the coupon. Since neither the ECB nor IMF has real investors, they could extend the maturity. Since the ECB bought many of the bonds below par, they could forgive some debt and still not have a loss versus their purchase price. I think the EFSF has less flexibility to take an immediate write-off, but I’m told in this game of three card monti and hide the loss, that is everyone’s favorite choice.

So there is a lot that the EU, ECB, IMF, and even EFSF could do to help Greece. Yet there has been a lot they could have done for awhile. They have been completely unhelpful. They have drawn lines in the stand and been adamant about not taking any haircuts.

So the only way to really help Greece out is to take some OSI. Official Sector help has to come. But what will that mean?

The IMF seems the most willing to play the pretend and extend game. They could extend the maturity and lower rates. Americans are too caught up in the election campaign to focus on the fact that it is in a large part, our money that the IMF is playing with. If Europe also plays their part, then I think the IMF will get away with it, but if the IMF is the only one to offer better terms, I think we could see a real backlash, both here and abroad. I’m not sure China would be happy to see their IMF money being used frivolously when Europe won’t share in the pain on their direct support.

It could come down to the IMF acting alone which would be reasonably helpful, but I don’t see it happening as too many countries that support the IMF would have a tough time at home explaining why they have to be more supportive of Greece and Europe, than Europe is.

But what happens if the EU or the ECB or the EFSF actually have to take losses?

The ECB is highly levered. They have been making a lot of money on the SMP program, but have been paying it out to the various national central banks. They are making a lot on LTRO as well, but aren’t retaining it. The ECB could write assets down to cost without booking a loss (as I understand their accounting), but that is less help to Greece than it would have been a year ago (the ECB has been the biggest beneficiary of the past 12 months of new Greek bailout money). The ECB cannot afford real losses without making capital calls. I cannot imagine the ECB making capital calls at the same time it embarks on OMT for Spain.

- Dear Germany, France, and others, we will need you to contribute your pro-rata portion for the €[10] billion loss we have taken on our Greek bond holdings purchased via SMP, but are happy to announce that OMT will be launching next week and we will make back much of this loss based on our purchases of Spanish bonds and can ensure you in the strongest words possible that we will never have any losses on those bonds.

This is why the ECB is stuck in terms of how much it can do. It has plenty of income, but it cannot show a big loss on existing bond holdings while trying to embark on another bond purchase program.

The EU and the EFSF have similar issues. Up until now people can complain about the bailouts, but until now it has been off-market rate loans. That is really all it has been. There hasn’t been any true transfer. Germany hasn’t lost a single pfennig (so far it has made money) but if that changes, expect opposition to mount.

Hollande is passing implementing some bizarre budget of his own, but last thing he needs to do is cover a few billion of losses on existing loans to Greece. It is the only way to help Greece, but it will make the anti-bailout crowd more vocal.

Across Europe, the reluctance to participate in the bailouts has been increasing. Leaders may finally be realizing they have done too little, but their population (i.e., voters) has been growing more disillusioned and taking actual losses will add to that resistance.

So I see Greece as once again being a focal point for the crisis and think that just like their eventual default last year, there is no good path. Some small attempts might be made, which may succeed briefly, but at this stage, the risk of a bad ending – either through failure to help or helping in such a way that the unintended (but obvious) consequences in Spanish and Italian bonds cause even greater problems.

The Scylla and Charybdis of how to restructure Greek debt in a way Greece can survive, without sparking another route in Spanish and Italian debt. If there is any group that I’m confident won’t figure it out in a timely manner, it is the EU and Troika.