Pre-Crisis LIBOR – Facts and Details

Pre-Crisis LIBOR – Evil but Miniscule

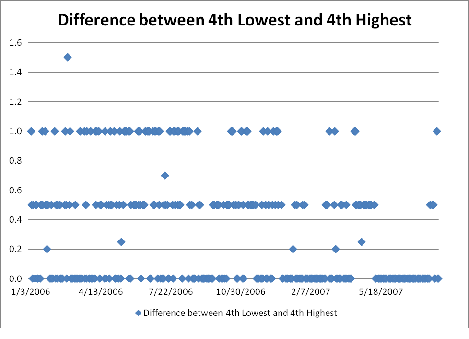

This is the most important chart of “pre crisis” LIBOR. I take the submissions from all 16 dealers, every day and compare the 4th highest to the 4th lowest. Neither of those data points would have been used, so it is an absolute maximum influence one dealer could have. If the stars aligned perfectly, one dealer could affect the LIBOR setting by that range divided by 8. It is hard to do, but in theory one person might be able to change the setting by the range divided by eight, but that would take a lot of luck rather than skill as it would depend on all the other entries.

From January 2006 until August 2007, there was one day that range was 1.5 bps. So with unbelievable luck, a single dealer might have been able to move LIBOR by 0.001875% so by almost 0.2 of a bp.

The average range from the 2 submissions that just got excluded was 0.3 bps making it possible for 1 dealer to impact the settiing by 0.000040525% on average if they got it perfectly.

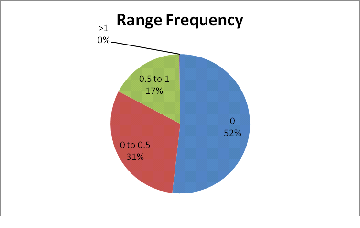

So 52% of the time during that period there was no difference including all 8 used submissions and the one excluded for being just too low, and the one excluded for just being too high.

If I only look at the submissions that were used, then the max range is only 1 bp and the average range from lowest included to highest included is 0.21 bps. Again, a dealer can only influence the outcome by an 1/8th of that.

Conclusion

It is clear from the FSA documents that Barclay’s tried to manipulate the LIBOR setting. It is clear from following up on specific days listed in the findings that Barclay’s was unsuccessful at moving LIBOR. You can see why. It was almost impossible to move LIBOR because all the submissions were in an incredibly tight band. People can talk about moving LIBOR via manipulation, but the reality is that so far this is no evidence of a bank being able to move it more than a fraction of a bp, and the data for the entire period supports that.

Collusion

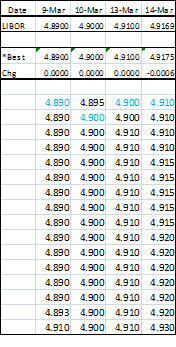

This is far more interesting as it might be possible that several dealers all moved their prices at the same time. If 8 dealers all moved 1 bp, then there would not be a big discrepancy and LIBOR would be impacted by a full bp. That seems hard to co-ordinate since banks would generally not want too many (any) other dealers to know their position, and having that many banks lined up on the same side of a setting on any day seems unlikely. I’m thinking of ways to test for it, but in meantime I took a look at March 13th, 2006. This was a day, according to FSA, that Barclay’s wanted to skew LIBOR lower.

If there was “collusion” I would have expected to see not only Barclay’s submit a low rate, but them to get several others to submit a low rate. Yet on the 13th, 1 other bank also submitted 4.9, but that was the bank that had been at 4.895 the prior day, so they moved in the opposite direction of what Barclay’s would have wanted, and it is reasonable that they were still at the tight end. Every other dealer went from 4.9 to 4.91 so no evidence of collusion there either. Especially since Barclay’s says the 91 is the “right” rate in the email where they agree to submit 90.

The manipulation was UNSUCCESSFUL as 4.91 was the rate which wasn’t influenced by Barclay’s submission.

The next day, one that the FSA doesn’t mention, Barclays raises its submission price, but remains at the low end. In theory had Barclay’s submitted 4.92, in line with other “wide” dealers, it could have caused LIBOR to be “off” by 0.0006%. Ie, a setting of 4.9175% instead of the actual one of 4.9169% (but maybe that day Barclay’s thought 4.91 was right rate, we just don’t know).

For the record, that would have cost someone $157 on a $100,000,000 trade if it was manipulation. You can’t get a lawyer to spell lawsuit on a piece of paper for $157.

Look at Variations during Crisis Times

The e-mails are damning. People should lose jobs. There should be fines. I doubt there will be many big lawsuits based on pre-crisis manipulation. Manipulation during the crisis is another story entirely, and one for tomorrow.