The T Report: La Eu et Le ECB sont á Faire la Lessive

Cleanest Dirty Shirt, Decoupling, or Two Ships Passing in the Night

There are a couple of common refrains I hear and read about a lot lately. The theme is that the U.S. is the “cleanest dirty shirt” or that the U.S. economy is “decoupling”. What if that is already priced in and no longer true? What if Europe is finally getting its act together? For so long, investors have become accustomed to disappointment after disappointment out of Europe, that maybe we are blinded to any actual progress being made. Maybe the EU and the ECB are doing the laundry, and while the shirt still has some nasty stains and disgusting ring around the collar, it’s just possible that our shirt is now dirtier.

What if we are decoupling, but where Europe is finally turning the corner and the attention is about to focus on our problems. Our budget fiasco, the fact that the Fed is saving the government about $100 billion a year through its questionable policies, that getting anything meaningful done on the fiscal cliff is less likely than New Gingrich starting a moon colony? After years of complaining about Europe, are we prepared for some fingers pointed at us? There are more and more politicians and heads of big international agencies (like the IMF) willing to say negative things about the U.S. politics.

While we enjoy the 4th, comfortable in our superiority and that we are cleaner and have decoupled, it’s quite possible we are like 2 ships passing in the night, and that soon the focus will turn on us.

Is Too Much Priced In Already?

Whether the decoupling theory is accurate or not is less important than determining if it is already fully priced in. If it is fully priced in, then it won’t take much of a change in perception to create large moves.

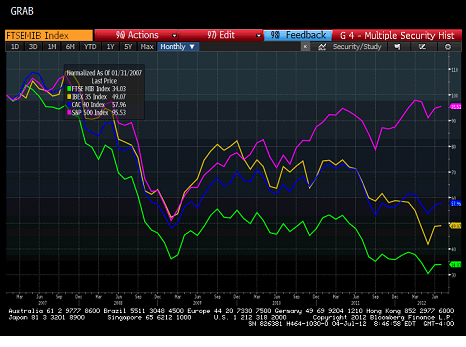

Since the start of the global financial crisis back in 2007, the S&P has rebounded almost completely, yet France and Spain remain around 50% of their 2007 levels, with the Italian index at not even 35%. I have ignored the impact of currency, but with the EUR down from 1.31 at the start of the period to 1.26 now, that only makes the decline worse.

Looking at the moves on a shorter timeframe doesn’t change the story much. Since the start of 2010, when you could argue that Greece started the European Sovereign Debt crisis, the markets have diverged significantly. The S&P is up almost 25% since the start, while Spanish and Italian stocks are down about 40%. France is “only” down 20%. That is a meaningful outperformance by the U.S. markets, and over that time the Euro moved from 1.43 to 1.26 so the loss of value in Europe is even bigger than that.

Even on the bond side, we see a similar reaction. German and American 10 year bond yields have moved roughly in lock-step. France has decoupled little, but only recently, while Italy has long since separated from the pack. We all know the reasons why these moves make sense, the question is, are they overdone?

And even the much maligned CDS market shows this. Europe typically traded tight to the U.S. (in part because it had more financials). During the early stages of the crisis the U.S. CDS index traded ever wider. It has since reversed and Europe is trading much wider than the U.S.

Whether the decoupling theory is accurate or not is less important than determining if it is already fully priced in.

Is it Time to Bet on Europe versus the US?

I’m not about to fully endorse that trade, but it makes sense on many levels.

- Europe is trying to address their problems, more seriously than ever, so shouldn’t the assets receiving the most direct help benefit the most, rather than generic “risk on”

- The outperformance has been very clear and may no longer be justified (if it ever was in such a global economy)

- The U.S. has its own set of warts that may finally become the focus, so while the problems won’t be new, the focus will, and that could spook risk takers. I find it hard to imagine that the rhetoric from politicians will become less caustic as we move towards the election.

- Earnings for the first time in recent memory seem set to disappoint along with the economic data, pinning more of the market valuation on hopes of QE. There is a chance that the Q2 data was as understated as the Q1 data was overstated and the slowdown wasn’t as pronounced as it appears, that is a tough one to believe with such overwhelmingly poor global data

For now I remain long biased. Though have started taking off risk in the U.S. and leaving it in Europe. I still like banks here on the back of what I expect to be some positive news, but the LIBOR scandal isn’t helping that trade.

Investment grade credit, particularly IG18 seems overdone, as now the index is trading 6 bps rich to fair value which is an indication that hedges have been cut and longs set. I think that IG18 will struggle to go much tighter without single names catching up, so it would be a decent short.

HYG is again beginning to look frothy as it is closed at 91.2, which is a 1% premium to fair value, but with so little high yield issuance, tremendous monthly coupon flows, central banks globally committed to ZIRP I think it is a bit early to be short this, though would be starting to cut back positions. In high yield, the next move higher will have to come from a shift in allocation to less liquid bonds and “story” credits as there just isn’t that much room for high coupon yield to call bonds to move and the longer dated high quality bonds are too sensitive to treasury rates here to move much higher in price.

Just food for thought, but it may be a good week to contemplate what is priced in, and if you are buying S&P because Europe is getting fixed, maybe it’s time to buy Europe since that is the market getting fixed.

This last chart is from yesterday, and doesn’t look quite so good with today’s weakness in Europe, but for all the angst over Italy this year, most investors who bought Italian 5 year bonds and have held them have positive year to date returns. Just seems a bit surprising relative to the barrage of non-stop negative headlines.