Europe Fighting the Wrong Battles Again with Dangerous Consequences

Europe continues to fight the wrong battle, and continues to spread contagion risk.

It is clear that Greece has had a solvency issue now for over 2 years. The ECB and Troika chose to treat it as a liquidity problem. Maybe, they could have argued that in early 2010, but by the summer of 2011 it was obvious to any credit observer that the problem was solvency, yet they continued to treat it as one of liquidity. That is scary because if they feel to see the problem correctly now, they will fail miserably. Not only is the problem clearly solvency, but now forced currency conversion has been added to the mix. Any “solution” from the EU must now address that risk, and it is not the same as solvency. Programs that can protect against solvency may do nothing for the redenomination risk.

Not only did Europe fail to address the problems, but in spite of convincing themselves that all these programs prevented contagion risk, they actually ensured contagion risk. That contagion risk, that they forced on themselves is now coming back to haunt them, and must be carefully addressed in any policy “solutions”.

Two Years of Bad Policy Have Created a Situation Like No Other

There is a lot of talk about what a Greek exit would or wouldn’t look like. People are comparing it to other defaults and currency devaluations. They are wrong. Greece is now unique in that almost all of the debt is owed to institutions that normally step in after devaluation. Greece is also unique in that it is leaving a currency union that is already fragile, and being the first to leave will open the floodgate of speculation as to what other countries will leave.

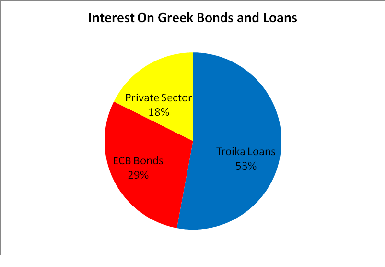

Greece is running a primary deficit, but that doesn’t make its interest payments any less important. Greece has €150 billion in loans, roughly half of which seem to be at 4% and half seem to be tied to PSI, so I conservatively assumed 2% on those. About €4.5 billion of interest is being paid to the Troika annually on these loans. The ECB (and EIB and other central banks) hold approximately €50 billion of bonds at about 5% average coupon for another €2.5 billion of interest. True “private sector” holders of Greek debt only receive about €1.5 billion. Most goes to pay the €66 billion of 2% coupon PSI debt and the rest is for the €4 billion of holdout English law bonds. I did ignore the €14 billion of t-bills in this analysis.

It is very obvious though, that for Greece to get any help on its current interest expense it has to cut back on the Troika and ECB in particular. Over 80% of its annual interest expense now goes to pay government and quasi governmental entities.

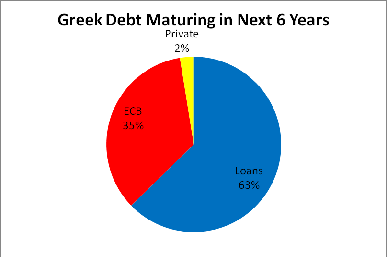

It’s not just the interest payments that are heavily skewed towards the Troika, it is also the debt redemptions that Greece is facing. A staggering 98% of all debt redemption in the next 6 years goes to pay off the Troika and ECB, with the ECB’s remaining bond portfolio representing 35% of the total, and almost all of the payments in the next 3 years.

Never has there been a situation where a country is in such deep trouble that it needs to default and virtually all of the debt is already held by entities which normally step in AFTER a default and currency devaluation.

Damned if You do, Damned if You Don’t

If Greece defaults or restructures or reverts back to the Drachma without forcing the Troika and ECB to take a hit, then Greece is doomed to another round of defaults, likely within the year.

Speculation is that a return to the drachma would result in a 25% to 50% currency devaluation. Just forcing the private sector to convert their debt to the new currency does almost nothing for Greece. The interest burden of attempting to pay Euro denominated debt with devalued drachma’s would be impossible. The redemptions would become unbearable. Greece cannot revert to a drachma without immediately affecting the Troika’s holdings, or defaulting, likely within a year.

This is where it is so different than any other situation we have seen in the past. There is no private sector to take the hit. The private sector already got wiped out with PSI. Germany and the ECB should have made concessions then, but chose not to. Now they are in a situation, where less than 3 months after a massive private sector hit, the horrible plan is already falling apart, and Greece needs immediate relief, or needs to leave the Euro.

So far Germany in particular has kept to the “austerity” and “original plan” line. Neither the ECB nor the IMF have done much for Greece, but at least don’t seem to be as belligerent or as antagonistic as Germany. Rather than arguing why Germany, the ECB, and IMF should rework the plan, I will look at the logical consequences of failure to do so. I think the potential risk of forcing a “Grexit” at this stage will become too obvious and be too large for the EU to risk it until better policies are put in place.

Direct Impacts of Greek “Drachmatization”

If Greece returns to the drachma there is a real risk that trade will break down. How will companies be treated? What happens to contracts that Greek companies made? Will they be honored in original form or also be subject to being redenominated? Can Greek companies afford the contracts after introduction of the drachma? This is just basic stuff, but in a world that depends on global trade, it is hard to tell what the consequences of a trade breakdown with Greece would be. We saw from the Japanese earthquake how sensitive and widespread problems from seemingly isolated supply line problems can develop.

That is all based on the hope that the world doesn’t become fixated on a chaotic breakdown of Greek society. The worst case is shortages of fuel and food where prices skyrocket in the immediate aftermath of the redenomination. Industry grinds to a halt from a lack of raw materials. This should be the easiest element of a devaluation to deal with, but it will require planning.

I’m assuming that depositors will be forced to accept drachmas in their bank accounts rather than keeping Euros. If they are allowed to keep Euros, then the situation would be better, except for the fact that the already insolvent banks would become more insolvent if forced to pay out depositors in Euros while have most of their assets turned into drachma.

These problems are unlikely to get out of control, and should be “merely” disruptive but would benefit from planning and preparation, none of which has really occurred yet.

Bank runs in Italy, Spain, and Portugal

This is the most likely result, no matter what happens to the ECB, IMF, and EFSF’s positions.

If you have a deposit in a bank in a country at risk of redenomination, then you would have to seriously consider taking money out to avoid that risk. This isn’t default risk. This is different. You aren’t concerned that your bank is going to default you are concerned that €1,000 will turn into 1,000 lire or pesetas of unknown value. Pan-European deposit insurance will NOT stop that flight of depositor money, unless it also ensures against forced conversion. That is a big risk to insure against, and may not be even remotely in the ECB’s mandate. So this is another difference from any other situation. If Argentina devalues, there is always risk that Brazil would devalue as well. That contagion risk played out in Asia in the late 1990’s. That risk is amplified here, because Greece will be a template for the others. In the back of every depositors mind, will be the fear that their country does it too.

I am scared that the ECB thinks they can address that risk with liquidity measures because they cannot. I am scared that the ECB thinks they can address that with solvency measures because they cannot. Real fear of forced currency conversion and devaluation is a new fear and new problem. You may not be concerned that BBVA is going to default, but you may be afraid that your account will be turned into something worth a lot less.

The only way to stop this is to insure against it (difficult) or to force Greek banks to pay depositors in Euros. But it is unclear how the Greek banks could afford to pay people out in Euros. The banks are already insolvent and the amount of additional money they would need to pay depositors in Euros would just push the problem elsewhere into the system.

I don’t see an easy way to stop a run on the banks in any of the weak countries if Greek depositors are forced into Drachma, and I don’t see any way for the Greek banks to pay depositors in full in Euros.

Anticipating what forced currency devaluation would really do is a new aspect to the crisis. It isn’t a liquidity or a solvency problem, it is its own problem. Politicians and central banks have to focus on this issue. I remain afraid, that like at so many other stages in this crisis, they will fail to understand the real problem, so their “preparations” will fail to stop this run and the crisis will escalate.

ECB Losses and Contagion

What will the ECB do with their losses? This seems to be a case of being stubborn and foolish. The ECB is not a mark to market entity. It funds incredibly cheaply and can print money. I remain convinced that it would cost the ECB much to convert their existing Greek bonds to PSI bonds at cost. With the debt maturity schedule that Greece faces, this would be a big benefit and would take a lot of pressure off the governments. Not the pressure to implement reforms, but the pressure that is killing the economy.

If Greece leaves, what is the ECB really going to do? Do they really expect Greece will pay them back at par in Euros with their new weak currency? That is stupid. Will the ECB print money to make up for the losses? That is one possibility, but given how stubborn Germany has been about austerity and how they hate printing money even more, I expect that the ECB would not print money to cover the losses.

If the ECB is going to take a loss and won’t print money, then they would have to go to their members and ask for more money. That seems highly unlikely, especially if Spain and Italy are busy trying to prevent a run on bank deposits. So, sadly, the plan seems to be to sell the bonds to the EFSF at either cost or par and let the EFSF take the loss.

Feeding more losses to the EFSF starts to fan the flames of contagion. The EFSF will have losses on its own loans, but now for the first time, obvious to everyone, the EFSF will be just a loss transfer mechanism. It will pay good money for garbage and then ask the EFSF members to pay for it. Because of the guarantee program they may not have to ask Germany and France for money right away, but the pretense that the EFSF guarantees don’t count against a nation’s debt burden will be shattered.

Attention will quickly focus on how much new money Spain and Italy are on the hook for. They are both contributors, and Spain will be dealing with regions that are running out of money, and both will be dealing with full fledged banking crisis of their own.

The scam that guarantees don’t count will be exposed. Spain and Italy may even need EFSF money by now. Investors will be thinking about the €160 billion or so of Spanish, Italian, and Portuguese debt sitting on the ECB’s balance sheet and wondering what is going to be done with that? Who is going to take the loss on that pile of bad debt?

Everywhere you turn, you will see exposure that was never accounted for and is getting worse. Some Bundesbank official will blabber on about not printing money and the market will become dizzy with fear. The ECB’s bond portfolio turns into losses for the EU. The EFSF turns into losses for the EU. Spain and Italy will need money from the EU for their own problems. The EU is just Germany and France. They don’t have the money. Pandemonium ensues.

Maybe it won’t be that bad. The ECB will launch LTRO3, but given the half life of LTRO2, that may do nothing to quell the fears. Actually, depositors and bond buyers in banks that used a lot of LTRO money will become scared of solvency. The LTRO helps banks last longer, but any bank that defaults will have incredibly low recoveries for unsecured lenders. The ECB will have all of the collateral, which will be declining in value requiring ever more to be posted to the ECB and less there for general creditors.

Just because the LTRO worked the first 2 times, doesn’t mean it will work a 3rd time, especially since its flaws have been exposed.

Simply put, the ECB should negotiate a better deal with Greece now, rather than risk this potential turn of events, and pretending that EFSF doesn’t actually create contagion is naïve.

Crumbling IMF Firewalls

The ECB won’t be the only entity to lose. The IMF will too. The IMF is more senior, but will they really be able to enforce any of their rights? This is also where the problem is completely circular. Greece will need IMF money to function. The IMF’s primary function is to ensure a country on the edge can get the funds they need. So the IMF will be the biggest existing creditor, but also the most likely future creditor. What a mess.

A self-made mess since the IMF traditionally forced defaults before lending. Remember back in 2010, the IMF changed its policy for Europe and didn’t really force them to do anything to private lenders before stepping up? They had those policies in place for a reason, precisely to try and avoid this sort of situation.

Then there is Lagarde’s precious firewall. Do you think she told any country they might have losses on old loans within 2 months of agreeing to this new and bigger firewall? I think a lot of people pledged their support because it seemed costless and were assured that the IMF never loses money and would likely never need this money.

With Greece, the IMF will lose money in the initial devaluation, or when Greece defaults because they played hardball. With countries witnessing the losses, and seeing the risk that any “firewall” contributions to Spain and Italy go down the tube as well, the reluctance to live up to pledges will grow.

The IMF could try to impose very strict terms on Spain and Italy for “firewall” money, but then it is highly unlikely it will really be of much help, and will just once again shift around who bears the ultimate cost.

The IMF, another entity without anything resembling a real world P&L might just be tempted to cut the interest payments and extend the maturities on its existing loans to Greece and others. If not, look for the fabled firewall to be just that – a fable.

They See the Light or Dark Bottomless Pit

I keep playing with scenarios and find it hard to find out where a Greek exit doesn’t result in a steep sharp decline in the market. We could go through more ideas of ECB intervention, but in the end most will have flaws. Dealing with currency conversion risk is huge. Dealing with the contagion risk that has been created by the EFSF is huge.

I believe that as they start to plan, they will eventually listen to some of the “doomers” and decide that they should attempt some policies to retain Greece for now. To fix the situations in Spain and Italy so that a return to the drachma isn’t likely to spark fears that Spain and Italy will also redenominate.

Can Greece leave and the damage be contained? Sure, it’s possible, but seems highly unlikely. Can Europe do enough to keep Greece in for another 3 to 6 months and make plans that make an exit controllable or possible avoid an exit altogether? That is possible, and seems a better solution. Will Europe force Greece out thinking they have a plan that fails miserably and sparks the miserable series of consequences I’ve outlined? Sadly, yes.

E-mail: tchir@tfmarketadvisors.com

Twitter: @TFMkts