What the TF? New Greek Govt Looks at Old Govt’s Debt Deal

In a world full of unintended consequences (where unintended invariably means bad) the profile of the Greece’s debt is interesting.

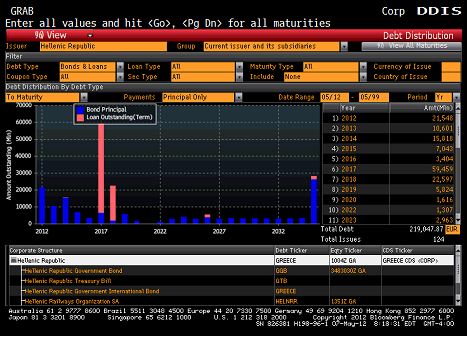

Greece currently has €220 billion of debt outstanding. That will grow as part of the “bail-out” but since the bank recapitalization isn’t done, and other money has been held back, the amount is smaller than the final projected amounts.

Troika loans are about €77 billion of this amount. These loans have stricter language and will be hard for Greece to do much about.

Of the €142 billion in bonds, at least €50 billion are the ECB’s holdings (remember, they have been getting paid off on bonds as they mature). This amount should draw the attention of the newly elected Greek government. While the Troika loans may be tough to walk away from, these bonds, held as part of an ill-advised secondary market purchase program would be a nice target for more debt reduction. In fact, it looks like over €3 billion is due to go to the ECB this month. Think about that. This newly elected government has to borrow €3 billion from the ECB to pay back the ECB? It has to be tempting to renegotiate with the ECB and make them take some share of the losses (especially since they have been earning interest, getting paid par on bonds already matured, and didn’t pay par for these bonds in the first place). This disagreement between Greece and the ECB is why the ECB has not been involved lately in the secondary markets recently, and why that role is being pushed onto the EFSF and ESM (if and when that is implemented). Watch this.

Of the €90 billion or so of private sector held bonds, the €450 million due on May 15th are particularly interesting to watch. An actual default on these could lead us right back to the “disorderly” default scenario that so many people were afraid of. Although I don’t think a default would be a disaster, much of the market thinks it would, so I suspect Greece will pay off these holders. The next maturity isn’t until June 2013, so I’m guessing all parties will suck it up and pay these holders out so they can put off more decisions for a bit. What that does to the game theory analysis when other countries start their own PSI, I have no idea, but suspect it doesn’t make it easier for countries to achieve their goals.