The Weekly Update – NFP and 50 DMA For S&P

In a very thin market, the S&P futures came very close to hitting their 50 DMA on Friday. The S&P futures went from a high of 1,418 on Monday, to trade as low as 1,372 on Friday. A 46 point swing is healthy correction at the very least, if not an ominous warning sign of more problems to come.

There were 3 key drivers to the negative price action in stocks this week. All 3 of them will continue to dominant issues next week.

Spain and Italy

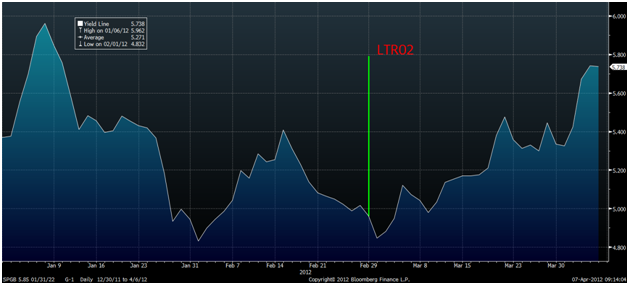

Spanish 10 year bonds hit a low yield of 4.83% in early February. They sold off from that level until the anticipation and execution of LTRO2 drove them back to 4.85% on March the 1st. They struggled from that point on, in spite of equities in general, and even more of the credit market doing well. It was a canary that was largely ignored, until the week of March 20th. Then people started noticing the problems in Spain. Budget deficits that continue to miss targets, staggering unemployment rates, and problems at the regional levels (in Spain, the regions are responsible for healthcare, not the central government – one reason why debt to GDP at the national level looks okay, but also why the problems at the regional level are very serious).

The “firewall” talks helped calm the situation, but the incongruence of Spain having to issue debt, to be part of a “firewall” to issue more debt, to go and buy Spanish debt, finally hit the market, and the selling pressure resumed. The 10 year bond has the least support from the LTRO program. Even the most aggressive Spanish banks will be reluctant to take on 10 year debt, when their funding gift only lasts 3 years, plus they would be obligated to post variation margin on assets pledged against LTRO borrowing.

I see no reason, away from EFSF or ECB purchases for the Spanish 10 year bond yield to find support. Too many aggressive buyers stepped in, under a mistaken belief of what LTRO could accomplish, and misjudging just how illiquid these markets can be. The weak auctions were a wake-up call (and may also be a sign of what happens to bond auctions of weak countries, once CDS buyers have been scared into submission). Many of these “come lately” investors used leverage to attain 10% potential returns. They are trapped, but the selling in 5 year has accelerated. Last week, the 10 year yields moved 40 bps, but the 5 year yield moved 46 bps. Even more surprising, and far more concerning was that the 2 year bonds actually move 46 bps and went to almost 3%. These are at the heart of the “LTRO fixes the sovereigns” analysis. That they struggled so much is a very serious issue.

While the problem remained isolated to the longer maturities, you could think of some “easy” remedies, like longer LTRO. With clear signs that even LTRO can’t hide the problem forever, the ECB may have to come up with even more creative solutions, and that will take time, especially as they try and transition more responsibilities (loser trades) to the EFSF, and many question how counterproductive ECB holdings were during the Greek restructuring.

Italy has moved out as well. Not quite as much as Spain, and as much in sympathy as any specific new concerns. Portuguese bonds also finally had a significant down week. Somehow, investors had bought into the Greek restructuring/default as being unique, but now there is once again a growing realization, that some austerity, mixed with some programs to promote growth, only really work if the debt burden has been reduced in the first place.

Non Farm Payroll

A number that would have excited the market in January seemed to spook the market on Friday. It was only futures, and a shortened session at that, but the reaction was swift and painful, with futures indicating a potential 1% loss on the open Monday if nothing changes between now and then. I’m a little surprised how strongly the market reacted (and took off some shorts), as I expect we will see at least one solid attempt by the QE is back on the table crowd to push markets higher.

We have believed that great weather and some extreme “seasonality” over the past few years made the January and February numbers seem much better than they really were. We had some hope, that the spike in jobs would “jump start” the economy and encourage more hiring, but felt the adjustments had overstated what growth there was, and that much of that growth had been because the weather had allowed a lot of projects to start early, and encouraged shoppers to be out and about more than in prior winters. I had been concerned that continued great weather in March would mean it would take longer to see this give back. It is once again concerning that we started to see the give back in a month where the weather certainly was a helpful factor.

We need jobs to get housing going. Housing is the key, and more jobs were supposed to lead to a rebound in housing. We never saw a real rebound in housing in spite of the jobs numbers, and now I think we know why. The job numbers were distorted, not the housing numbers. The hopes that housing would catch up to jobs seems to have been hit badly now. The reality is that jobs are falling back to levels consistent with the housing data.

The entire renewed and strengthened economic recovery story has to be questioned, and not just because of one number. Most of the numbers had led us to question the premise that economic growth in the US was on a stronger footing, and it was only the job numbers that made us question that. With jobs returning to mediocre, the view that the economy is still very fragile, has to be the main assumption.

QE3 or QED

Are we going to get another round of QE or are they done for now? That is a key question.

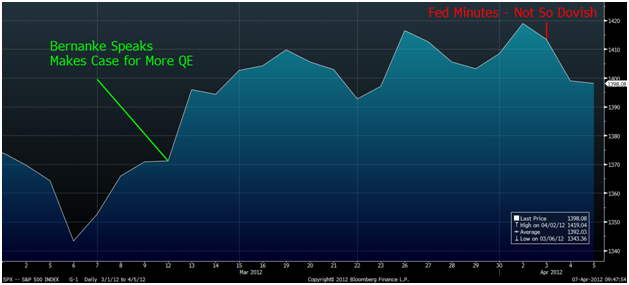

Two of the biggest recent moves were a direct result of the markets determining that QE was coming, or that QE wasn’t coming.

The Fed did what they are supposed to. They said that not only QE, but also short term rates are dependent on economic data. Assuming that short term rates will remain zero while we see improving economic data and signs of inflation (even if only in gas and food and things we need) is just as wrong as assuming that QE is off the table if the economy takes a leg down.

What really changed is the perception that Ben would be able to jam in some QE in spite of signs of economic growth. Ben has been trying to find ways to get “people” to focus on the negatives and the concerns so that he can justify another round of QE. The minutes indicate that the rest of the board is less willing to go along with that game. Ben can talk about Okun’s law all he wants, but the other members may have had enough and will be more patient about growing the Fed’s balance sheet or expanding into riskier assets (longer duration and/or mortgages). That shift may take time for the market to digest, and near term I think it is negative for rates, but also negative for stocks. In the end, it should reduce volatility in the stock market, as the market gets better at assessing the probability of QE since it will be more directly tied to economic data (it should no longer be at the whim of one man now).

What else to watch for?

So those are the stories that drove last week. They weren’t new stories, and in many cases people were focused on them, they just happened to be the biggest drivers. They will continue to be important factors in this week’s trading.

China remains a big question. They are “landing” but it is far from clear if it is going to be a soft or hard one. Data should be less confusing over the coming weeks as the impacts of the holiday dissipate. China seems to be taking on an ever increasing role in the world’s policies. They look set to step up their involvement and commitment to the IMF, but they also seem to be taking steps to influence our policy – they have questioned QE publicly – and also seem interested in ensuring that the U.S. dollar isn’t the sole reserve currency in the future. I continue to believe that the problems there are bigger than we realize, but that the official data is unlikely to admit to the true extent of those problems. A lack of clear direction from China is the base case for now, but I would look more for negative surprises, rather than positive ones from their domestic economy. The additional IMF support might be good, but I think we have rallied about 3,000 points on the S&P over the past year on Chinese support for the IMF, so don’t think there is a whole lot more to get out of it in stocks.

The situation in the Middle East seemed to have disappeared from the headlines this week. That could be a sign that the tensions have eased and there is less risk of a problem coming from there, or just that we had enough other things to keep our attention focused that we didn’t bother looking there much. I’m leaning towards the latter. Progress in the mid-East would be positive, but I think we see another round of escalation, and the rise in oil prices that go along with it, before it truly calms down.

The energy markets seem as confusing as ever. Natural gas is a disaster. Car gas is a disaster in the other direction. Government sponsored solar companies were a disaster. On one hand we could see the nation take comfort from secure, abundant, domestic supplies of energy and build on that. At the same time, with a few screw-ups here and there by the politicians, and some defaults by junior, highly leveraged nat gas producers and we could see another wave of delays and problems that hurt all of America.

Fixed Income Allocation

We only had a minor shift in our Fixed Income Allocation target. We took off 5% of the allocation to HY, and although we looked at adding that back on Thursday, HYG didn’t hit our price target. With Friday’s action we will be looking for opportunities to add back that 5%.

We also were in and out of treasuries. We had briefly put on a 10% allocation which we put back to 0%. So far it looks like we were too early in taking that off, but our theme of treasuries being more at risk to a swift drop in price (increase in yields) remains intact. High yield has sold off since we cut the allocation, and with our deep concerns about the debt problems in Europe, this asset class needs to be watched carefully.

Here is the allocation that we sent out last week and a more detailed analysis of what we liked and didn’t like.