The T Report: Two Types of Credit Losses

There are signs that the credit situation in Europe is deteriorating. Bond yields and spreads are worse across the board once again. Of some concern is that Italy is underperforming Spain a bit today, in CDS, the 5yr, and 10yr points. The “firewalls” can’t really handle Spain, but there is nothing to do if Italy becomes the focal point again. Curves are flattening again in Spain and Italy, with 2 year yields out almost 20 bps in each country. Two year bonds were at the heart of the LTRO, so their continued weakness is very concerning. The moves remain small (20 bps is barely 0.3% on a price basis), but the fact that weakness has seeped into the most “protected” part of the curb is a clear sign that the weakness is real.

The other warning sign I saw today is an increase in bid/offer spreads in Europe. Yesterday the big guys maintained ½ bp markets in Main, and only some weaker dealers resigned themselves to obscurity with ¾ bp markets. Today, some big dealers have shifted to ¾ bp markets and the hangers on have shifted to 1 bp markets. See here for our old description of how CDS Index trading works. Fast momo is probably killing it today. Dealers definitely widen bid/offer spreads sooner than they used to. Job preservation has become more important than bragging rights for who kept the tightest markets longer, but it is a clear sign that client activity is sporadic, and at least some dealers are caught off-sides.

Which leads right back to the two ways to have credit losses.

The one way to lose money in credit is when you buy a bond and it defaults. That is the way that comes to mind for most investors. This is by far the easiest to protect against. With enough analysis and care, you can avoid defaults. You can construct portfolios so that you are compensated enough on the bonds that work out, that you make up for your defaults. In any case, this takes time and can be managed, but is the easy part of credit trading.

The credit losses that are harder to control, are when you are forced to sell because the risk becomes too great. It is a subtle difference, but is the key driver. Investors buy too much of a bond because the perceived risk is low. As spreads widen and volatility increases, the perceived risk increases. This may cause them to cut positions and take “credit” losses. Whether or not the default risk has changed, the perception of that risk has changed and you get forced sellers. Hedge funds are a prime example. There are many ways to get to 10% returns in the credit markets, but one common strategy, particularly when risk is perceived as being low, is to lever up trades. If you think LTRO is solving everything, and there is no way credit is going wider, how do you get to 10%? You buy some 5 year Spanish debt at 4% and leverage it at least 2:1. As yields hit 3.5% you look like a genius. Not only are you getting “carry” but some nice price appreciation. But now as yields bak up to 4.6% what do you do? Your premise that LTRO saved everything is shaky at best. Bonds that you bought in late January at 101.1 are now trading at 98.6. That is a 2.5% loss, or over 6 months of “carry”. If you were leveraged 2:1, the loss is closer to 5%, and is still over 4% including accrued interest. It takes a lot of conviction in the world of monthly returns to ignore the fact that these same bonds traded at 92 back in November.

This is the “other” form of credit loss and is the one we are seeing right now. This really isn’t about default risk, it is about bad positioning. But as these investors cut positions, we will see the awful truth about liquidity in credit markets. It is almost always “one way” liquidity. On the way up, you can sell as much as you want at a price, but can barely buy any. On the way down, the opposite is true. As the price moves increase, the desire to cut position size increases, reversing the positively self-fulfilling cycle that started with LTRO1 and began to break down about 2 weeks ago. Then wait until people start having to hedge their CDS counterparty exposure risk (since that is still not exchange traded). That can drag the financials down as it creates new pressure on their credit spreads (totally avoidable if the regulators had put any of this on an exchange sometime in the 4 years since Bear Stearns’ demise).

I’m a little surprised that we haven’t seen any ECB intervention yet, so have to be a bit cautious on being too bearish here, but none of the signs are good. As I wrote yesterday, I think the EU wants to have EFSF assume the role of secondary market intervention, but in typical EU fashion, they haven’t managed to set it up properly yet. That likely happens early next week, and I think the ECB will hold off until then, unless we crack 6% on the 10 year yields before the EFSF is prepared to act.

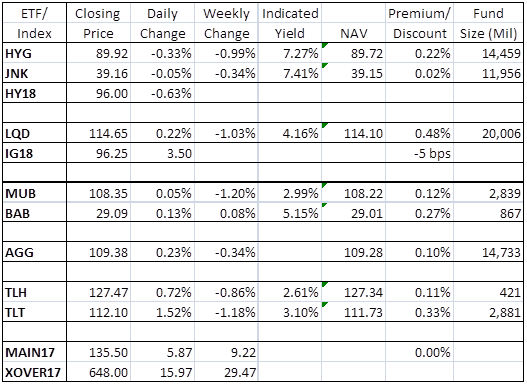

The TFMkts Best Ideas remains bearish risk assets, but will be looking to take that risk down today on weakness, and for the “fixed income allocation” strategy, are looking for opportunities to reload some of the HY risk we shed, especially since the premium to NAV is finally coming down.

IG18 is worse than I thought and is all the way out to 96 now, another indication of how poorly positioned people are for this move (the fact that it was trading so rich was the reason it seemed such an obvious short to us). This makes the late day trading that much more interesting. How to trade position ahead of tomorrow’s big NFP number when the US stock market will be closed?

I am having lunch with former Greek Prime Minister George Papandreou. I am really curious to hear why they have such an aversion to defaulting and rebuilding properly, and with some luck will be able to have some direct questions answered.